Maximum PayID Deposit Limits for Betting: Bank Ceilings vs Bookmaker Caps

A high-stakes punter messaged me during last year’s spring racing carnival with a specific problem. He wanted to fund a AU$40,000 PayID deposit at a bookmaker for a single race-day campaign. His bank said yes. His bookmaker said no. His bookmaker also said yes, just not at that amount in a single payment. He ended up making three transfers across a couple of hours and eventually the money landed.

Maximum PayID limits are where two different layers of caps collide. Your bank has one view of how much you can send. The bookmaker has another view of how much they want to accept in a single transaction. Neither layer is the same for every punter, and the interaction between the two is what determines the maximum deposit you can actually push through at any given moment.

Two layers of cap, working in series

The simplest way to think about PayID maximums is as two separate gates that every deposit has to pass through.

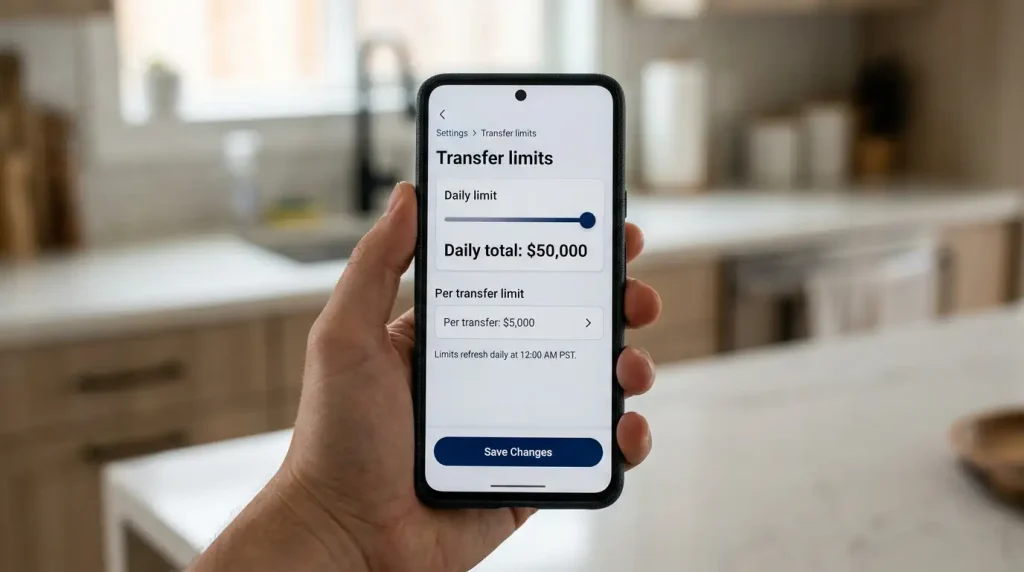

The first gate is your bank’s per-payment and per-day cap on outgoing PayID transfers. Every Australian bank sets some ceiling on how much a customer can send via PayID in a single transaction and in a rolling 24-hour window. These caps exist primarily for fraud-prevention reasons – if a customer’s account is compromised, the cap limits the damage a fraudulent actor can do before the customer notices.

The second gate is the bookmaker’s per-transaction cap on incoming PayID deposits. Operators set these for a mix of reasons: anti-money-laundering risk management, account-level verification requirements that apply above certain thresholds, and operational limits on how much funds can move through a single cashier session before triggering a compliance review.

Your maximum deposit at any specific moment is whichever of these two gates is tighter. If your bank allows AU$25,000 per transaction and the bookmaker allows AU$10,000, you can deposit AU$10,000 in one go. If the bank allows AU$5,000 and the bookmaker allows AU$10,000, you can deposit AU$5,000. The tighter cap wins.

The scale of the NPP rail tells you something about how these caps sit in context. Around 47% of registered PayID users transact through the rail at least weekly, and the rail as a whole handles more than 155 million transactions a month. Most of that traffic is small – consumer-to-consumer, consumer-to-business, ordinary daily spending. The bulk of PayID activity never bumps against any cap because it sits comfortably inside both layers’ limits. Large deposits are where the caps become visible.

Typical bank-side ceilings

Big-four banks set the broadest range of default ceilings. Commonwealth Bank, Westpac, NAB, and ANZ all apply per-payment and per-day limits on PayID that vary by account type and customer history.

Default per-payment limits at the big four range from around AU$5,000 at the lower end up to AU$25,000 on standard retail accounts. Daily cumulative limits sit in a similar band, typically AU$25,000 per 24-hour period for a standard transactional account before any customer-requested raise. These defaults are configurable – every big-four bank allows customers to raise their PayID limits up through an in-app process, usually requiring an additional security step like a phone-based OTP or a biometric reauthentication.

The upper ceiling you can reach at each big-four bank varies. Commonwealth Bank has been the most accommodating in my experience, with personal customers able to raise limits toward AU$100,000 per day with some paperwork. Other big-four banks cap raised limits somewhat lower. If you need to push a genuinely large deposit through, plan the limit raise in advance rather than at the moment of deposit.

Mutual banks and credit unions typically set lower default limits than the big four, often AU$5,000 to AU$10,000 per payment with daily caps in the same range. Some mutuals allow raises to higher levels; others do not. If you are funding a large bankroll, a mutual account might not be the right vehicle, and transferring funds to a big-four account before making the bookmaker deposit is often the practical move.

Neobanks vary widely. Some digital-only banks set surprisingly low default limits – AU$2,000 to AU$5,000 per transaction – reflecting their younger customer demographics and more conservative fraud posture. Others are more generous. The quickest check is in the app’s payment-limits screen, which every Australian bank surfaces somewhere in its security settings.

One detail worth knowing: the bank-side caps apply to outgoing payments to any payee, not just bookmakers. A AU$10,000 daily cap means you can send AU$10,000 total in a 24-hour period – not AU$10,000 per payee. If you are splitting a bankroll across multiple operators, the cumulative total across all operators is what matters.

Typical bookmaker-side caps

Bookmaker per-transaction PayID limits vary by operator and by account tier. Newly opened accounts typically have the tightest limits because the operator has limited history to assess the account against. Long-established accounts with strong verification records often have much higher ceilings.

The typical default per-transaction cap on a new account at a mainstream Australian bookmaker sits somewhere between AU$5,000 and AU$10,000 for PayID deposits. This is deliberately conservative. The operator has not yet seen enough account activity to determine what a normal deposit size looks like for you, and a large deposit on a new account is one of the patterns AML systems flag for enhanced scrutiny.

Established accounts can see caps in the AU$25,000 to AU$50,000 range per transaction, sometimes higher with specific operator agreement. Serious high-stakes punters who move large balances regularly will often negotiate bespoke arrangements with the operator’s VIP team – not because the rail itself cannot handle large deposits, but because the operator’s internal risk processes are more comfortable when large deposits are pre-discussed.

The ACIP verification framework that has applied since 29 September 2024 sits underneath all of this. A licensed operator cannot even open an account without completing identity verification, which means no large deposit ever lands on an unverified account. The framework makes large deposits safer for the operator to accept but does not eliminate the operational need for cashier-level caps.

Per-day cumulative caps at the bookmaker side also exist but are less commonly binding. An operator might set a AU$100,000 daily deposit cap against an established account but that is well above most punters’ realistic usage. The per-transaction cap is usually the gate you hit first.

One thing worth specifically flagging: the bookmaker-side cap can sometimes be negotiated upwards on request, usually through the operator’s VIP or priority customer channel. If you have a specific reason for a larger-than-standard deposit – a major race day, a pre-agreed syndicate contribution – reaching out to the operator in advance is often the fastest way to unlock the cap for a specific transaction.

How to lift a bank limit safely

If the tighter gate is your bank’s cap rather than the bookmaker’s, raising your bank limit is the practical solution. The process varies by bank but the pattern is consistent.

Open your banking app and find the payment-limits setting. The location varies but it is usually under Security or Payment Limits in the app menu. Most big-four banks let you increase the PayID limit directly in the app through a two-step verification process. Some ask for a phone call to confirm the change for limits above a certain threshold.

Raise the limit for the specific period you need. Some banks allow temporary one-day raises that automatically revert afterwards. Others set the new limit permanently until you change it again. If you are making a one-off large deposit, the temporary raise is usually safer because it narrows the window in which a compromised account could be exploited at the higher limit.

Do the raise before the deposit, not during. A limit raise that takes effect after your deposit attempt is too late for that deposit. Plan the process in advance – ideally the day before a time-sensitive deposit.

Do not attempt to bypass the limit by splitting the deposit across multiple payments timed close together. Banks’ fraud systems pick up on this pattern and often flag it as potentially fraudulent activity, which can result in all the split payments being held while an automated review runs. One well-timed limit raise is faster than three payments that each get flagged.

If your bank refuses a limit raise, the next option is to move funds to a different account that has a higher cap, then send from that account. This introduces a separate settlement step but can be quicker than waiting for a bank to approve a raise on a lower-limit account.

The 2024 credit card gambling ban – which took effect on 11 June 2024 and carries penalties of up to AU$247,500 for operators accepting prohibited payments – reshaped the funding landscape for large deposits. Before the ban, credit-card deposits offered an alternative high-limit pathway for some punters. After the ban, PayID sits alone at the top of the funding stack for large legitimate deposits, and the bank-side cap management process has become the main constraint bettors need to navigate. I cover the broader reshaping of deposit choice in the piece on the credit ban’s effect on PayID as the default deposit rail.