Source-of-Funds Checks on PayID Betting Payouts: What Bookmakers Ask For

The first time a bookmaker asked one of my readers for six months of bank statements, she thought she was being personally investigated. She had won AU$8,000 on a considered multi during the spring racing carnival, requested the withdrawal, and found herself staring at a document request that made her feel like a suspect. “They even want the deposits from my mum,” she told me. “She paid me back for the flights.”

That reaction is universal and completely understandable. The source-of-funds review is the most intrusive-feeling part of the licensed wagering experience, and nothing about the signup flow prepares a first-time depositor for it. What I want to do is demystify the process – what is actually being checked, why, and how to respond in a way that makes the whole thing end quickly rather than drag for weeks.

Why source-of-funds is requested at all

SoF requests sit inside a much bigger regulatory picture than any individual punter usually sees. The Australian wagering sector is rated medium-stable for money-laundering risk by AUSTRAC, which means it is under continuous supervisory attention. Every licensed operator is required to maintain ongoing customer due diligence, and the SoF check is one of the main tools in that framework.

The logic is mechanical rather than personal. When a customer withdraws a meaningful amount, the operator is required to be able to justify, from the records it holds, where those funds came from and how they entered the betting system. If the records do not support a legitimate source, the operator cannot release the payout without being potentially complicit in moving laundered funds. SoF requests are how operators build the record they are required to hold.

Triggering thresholds vary by operator but most begin generating automatic SoF requests somewhere in the AU$5,000 to AU$10,000 range for a single withdrawal, and lower cumulative thresholds for rolling periods. A punter who withdraws AU$2,000 monthly across half a year may trigger an SoF review even if no individual withdrawal crosses the per-transaction threshold, because the cumulative activity crosses the rolling threshold.

The broader AML context around gambling is significant. A former anti-money-laundering unit head at one of Australia’s largest clubs groups, Troy Stolz, has publicly stated that “between 20 and 30% of pokie revenue is money laundering.” That statement is about venues rather than online wagering, but the regulatory attention it has attracted flows through the entire gambling industry. Online operators run heavier SoF processes partly as a response to the scrutiny landing on the sector as a whole, not because online wagering specifically is thought to be a larger laundering problem than any other segment.

For the individual punter, this context is useful because it reframes the SoF request from “why me” to “this applies to everyone at this threshold.” You are not being singled out. You are being processed by a system that applies the same rules to every customer crossing the same line.

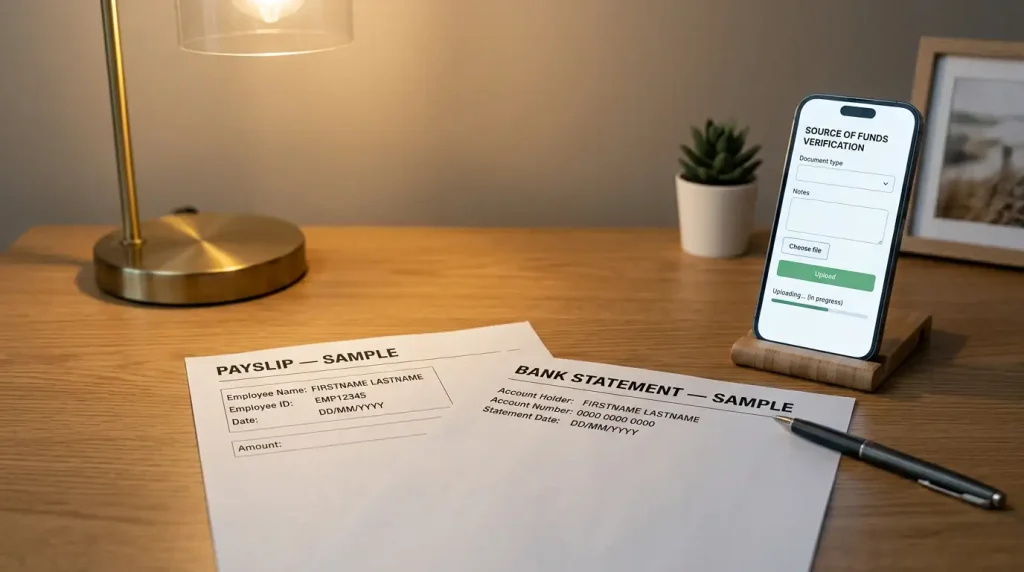

Documents usually requested

The document set varies by case but follows a consistent pattern. The operator wants to see a clean chain from an identifiable income source into the bank account your PayID deposits came from, and then into your bookmaker account.

Payslips covering a recent period – typically three to six months – are the most common starting point. The operator uses them to establish your baseline income and employment. A salaried worker with consistent payslips produces the simplest SoF pack. A self-employed worker, a contractor, or someone with multiple income sources needs a slightly more substantial document package.

Bank statements covering the same period are almost always requested alongside payslips. The statements serve two purposes. First, they corroborate the payslips by showing the salary deposits landing. Second, they let the operator trace the flow of funds from the income source to the bookmaker account. You will usually be asked for the account that your PayID alias resolves to, which is the account the operator’s inbound deposits came from and will pay out to.

For customers whose deposits exceed what payslips could plausibly account for, additional evidence is requested. Investment income statements, share or crypto disposal records, property sale settlement statements, evidence of an inheritance, or documentation of any other specific source of the funds. One-off large sources – selling a car, a bonus, a lump sum payment – are usually the easiest to document because the paperwork exists in one place.

For self-employed customers, expect to be asked for business bank statements and tax documentation. The operator is trying to reconcile business income with personal account deposits, and without business-side records there is often a gap the operator cannot close on its own.

The document I see punters get caught on most often is the bank statement showing deposits from family members or friends. The operator will usually ask you to explain these – who is the sender, what was the payment for. Honest answers are almost always accepted. Evasiveness extends the review.

How long the review takes

Review timing depends almost entirely on the completeness of your first submission.

A complete, clean document pack submitted in a single reply typically clears within one to three business days. The operator’s compliance team runs the documents against the pattern on your account, confirms everything reconciles, and releases the payout. I have seen clean reviews complete within hours for straightforward cases.

A partial submission triggers follow-up questions and can stretch the review to a week or more. The operator cannot resolve the case until all gaps are closed, and each round of additional questions adds a business day to the clock. If the operator asks for three things and you send two, the missing one becomes a ticket sitting in a queue, not an open channel for quick resolution.

A contested submission – where the punter and the operator disagree about what is required – can run longer again. Disputes over the scope of what is reasonable to ask for are real and sometimes valid. The resolution path runs through the operator’s internal complaints process and then, if unresolved, to the external dispute resolution scheme. I do not recommend starting a dispute until you have actually tried to provide what was requested first. Most SoF requests that feel unreasonable at first glance turn out to be standard once the context is explained.

My practical rule: block an hour. Gather everything the operator asked for. Check the format they asked for. Send one complete reply. Reviews close fast when the documentation is clean the first time, and the single hour you spend getting it right front-loaded is almost always less than the cumulative time a drawn-out back-and-forth would cost.

What happens if you cannot produce the documents

This is the hardest part of the conversation. Not every punter can produce a clean audit trail for the funds they deposited, and the reasons are often entirely legitimate.

Sometimes the documentation simply does not exist in the form the operator wants. A self-employed tradesperson paid mostly in cash, a retiree drawing down cash savings accumulated over decades, someone who recently inherited and deposited funds they have not yet formally documented – all of these can hit genuine walls in producing the requested pack.

In these cases, your options narrow but do not disappear. The first step is to open a direct conversation with the operator’s compliance team. Explain the specific gap. Provide what you can. Ask what alternative evidence the operator would accept. Many operators have flexibility in how they resolve non-standard cases and will accept substitute evidence if you engage constructively.

The second option is statutory declarations. A sworn declaration of the source of funds, backed by whatever partial documentation is available, can sometimes close gaps that bank statements alone cannot. Operators vary in how much weight they place on declarations, so check before investing in the paperwork.

The third, least palatable option is accepting that a particular withdrawal will not be released until the documentation is produced. This can feel punitive but it is not arbitrary – the operator is bound by the same AML framework regardless of how inconvenient its application is to any specific customer.

One path I strongly advise against: attempting to produce documentation that is not genuine. Fabricated payslips, doctored bank statements, and fake declarations are criminal offences under multiple legal frameworks and will almost always be detected by the verification services operators use. The downside risk is orders of magnitude worse than the withheld payout.

If you genuinely cannot satisfy an SoF request through legitimate means, the honest next step may be to accept that the specific amount will not be released and to adjust your staking pattern going forward so that future withdrawals stay within what you can document. It is not an ideal outcome. It is sometimes the realistic one.

For broader context on what happens when operators close accounts after disputes over funds or verification, I cover bookmaker account closures and how to recover your PayID balance separately.