PayID Withdrawal Delayed: Why AU Bookmakers Hold Payouts and What to Do

A winning punter messaged me in a state of quiet fury last spring. He had placed a good multi on a Saturday, cashed out a clean four figures on Sunday morning, and by Tuesday lunch was still staring at a “processing” status on his withdrawal. The operator was licensed, the account was clean, the PayID alias was correctly set. Everything looked fine. Nothing moved.

This is the most frustrating thing about PayID payouts in the Australian market. The rail itself is near-instant. The approval clock sitting in front of the rail is not. Understanding which one you are waiting on – and what the operator is allowed to do while you wait – is the difference between a reasonable queue and a complaint-worthy delay.

The types of holds you can actually hit

Payout holds fall into four categories, and the operator side does not always tell you which one you are in. Knowing the taxonomy lets you push in the right direction rather than sending generic “where is my money” tickets.

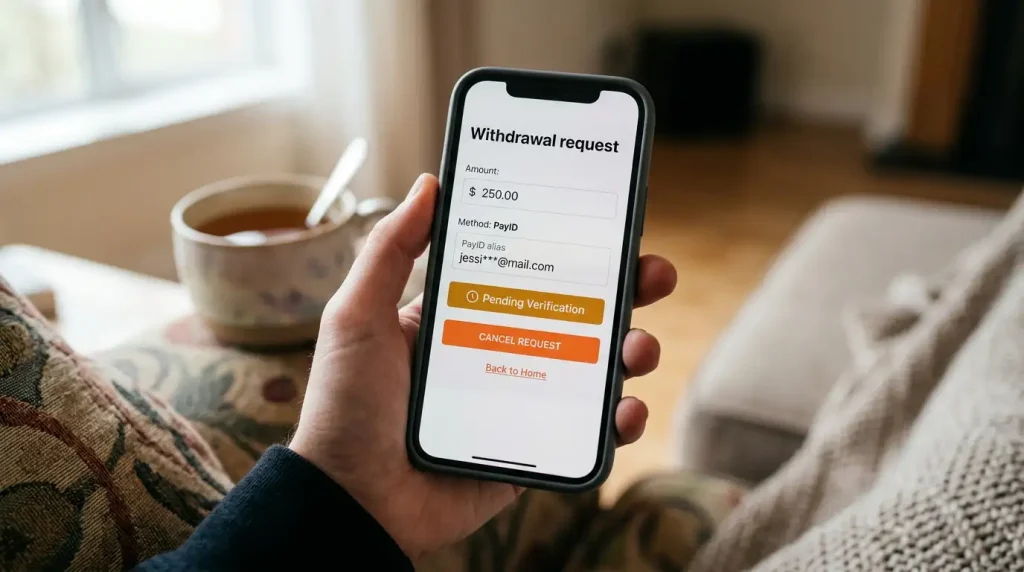

The first is the routine review hold. Every licensed Australian bookmaker reviews outbound payouts against a set of internal risk rules before release. For a clean account with a modest withdrawal amount, this is usually a matter of minutes. For larger amounts, for first-time withdrawals on a new account, or for accounts that have recently changed banking details, the review can run hours. This is standard practice and not grounds for a complaint.

The second is the verification hold. If your account’s identity verification needs a refresh – address change, ID expiry, a change in the account pattern that triggers an enhanced due diligence review – the operator will pause the payout until the check is complete. Since 29 September 2024, every licensed Australian provider has been required to run a compliant Australian Customer Identification Procedure before opening an account, and similar checks get repeated at specific trigger points through the account’s life. A verification pause can sit from a few hours to several business days depending on what the operator needs from you.

The third is the source-of-wealth hold. Withdrawals above a certain threshold – which varies by operator but typically starts somewhere around AU$5,000 – can trigger a request for documentation showing the source of the funds. This is AUSTRAC-driven compliance, not operator discretion, and it applies evenly across the licensed market. Until the requested documents are supplied and reviewed, the payout does not release.

The fourth is the dispute or flag hold. Any account that has been flagged for unusual activity, suspected collusion, bonus-term violations, or any other internal investigation will have payouts paused until the flag is resolved. These holds can run longer than any of the others and usually require direct communication with the operator’s compliance team.

The NPP rail itself, once the operator releases the payment, settles in seconds – the rail’s availability is engineered to tolerate downtime of no more than around two minutes per month, which for practical purposes means it is always on. If your payout is sitting for days, the holdup is not the rail. It is one of the four categories above.

Verification refreshes and source-of-funds requests

If the operator has asked you for documents, understanding what they are actually checking saves both of you time.

A verification refresh is the operator updating the identity record they hold against your account. Expected documents include a current photo ID – driver’s licence, passport – and sometimes a recent proof of address. The check itself is quick once documents arrive. The delay is usually in you getting them sent in a usable format.

A source-of-funds request is a different beast. The operator is asking you to document how you acquired the money you deposited, and sometimes how you acquired the funds you are withdrawing. Expected evidence includes recent payslips, bank statements showing salary deposits, documentation of investment proceeds, or evidence of a specific one-off source like an inheritance or a vehicle sale. This is the category where punters push back the hardest, and I understand why – it feels intrusive. It is also non-negotiable at licensed operators.

AUSTRAC is unusually direct about the posture behind these checks. Its CEO put it as bluntly as possible at a compliance conference: “This is a momentous time for AML/CTF regulation. We’re about to embark on the most ambitious overhaul of Australia’s anti-money laundering laws in a generation.” The operator asking for your payslips is not being difficult. They are operating under regulatory oversight that has sharpened considerably since 2024 and continues to sharpen through 2026.

My practical rule: if the operator asks, respond fast and completely. A partial response often triggers a follow-up request that adds another business day to the clock. Send everything clean, in one reply, to the specific email address the operator asked for. The check that was going to take three business days often finishes in one if your documents are clean the first time.

A separate article covers the detail of what bookmakers ask for during source-of-funds reviews, which is worth reading before your first large withdrawal.

What counts as an unreasonable delay

The reasonable-versus-unreasonable line matters because it is the trigger for escalation.

For a routine payout on a clean account with no verification queries, a reasonable PayID withdrawal window at a licensed Australian bookmaker is somewhere between a few minutes and 24 hours. Most licensed operators will release a routine clean-account payout well inside that window. Anything beyond 48 hours on a routine payout is worth a polite escalation ticket.

For a payout that has triggered a verification refresh, a reasonable window is one to three business days after you have supplied the requested documents. Count the clock from the time your documents landed, not from the time you requested the withdrawal. Operators legitimately cannot start the review until they have what they need.

For a payout that has triggered a source-of-funds review, a reasonable window is three to ten business days after complete documentation has arrived. This is a substantial piece of compliance work and the operator’s AML team is doing more than a cursory check. At licensed operators I have watched this process hundreds of times. Ten business days is the outer bound for a complete, clean documentation pack. More than that and you have grounds for a formal complaint.

For a payout held under an internal flag or dispute, there is no standard window. These cases are handled individually and can run weeks. They are also rare and usually attached to specific account behaviour – if you are not sure which flag is active, ask the operator in writing and keep the response for any downstream escalation.

The broader industry watchdog position, via ACMA’s own reporting, gives you a sense of scale: in Q4 2024 alone, ACMA investigated 301 complaints under the Interactive Gambling Act, found 16 breaches, and referred 75 sites for blocking. That workload exists because the regulator takes genuine operator misconduct seriously. A stuck payout from a licensed operator, with clean documentation, is the kind of complaint that gets attention.

The escalation path, in order

If you have hit what you think is an unreasonable delay, the escalation ladder runs in a specific order. Skipping rungs wastes your time.

Step one is the operator’s internal complaint process. Every licensed Australian bookmaker is required to maintain a documented complaints process, and you should ask for it in writing on day one of the delay. The request itself often unlocks the stuck payout because it forces a second set of eyes onto the case inside the operator.

Step two is an external dispute resolution body if the operator’s internal process has failed. Most corporate bookmakers are members of an external dispute resolution scheme and are required to tell you which one when you ask. The scheme will investigate on your behalf at no cost.

Step three is the NT Racing Commission, which is the licensing regulator for almost every corporate bookmaker in Australia. NTRC complaints are taken seriously because they bear directly on the operator’s licence conditions. This is a heavier step than it sounds and should be reserved for genuine operator misconduct rather than a slow payout queue.

Step four is ACMA, which regulates interactive gambling services at the federal level under the Interactive Gambling Act 2001. ACMA’s remit is primarily over unlicensed operators and specific conduct breaches rather than general payout disputes, but egregious cases do end up there.

Step five is AUSTRAC, which is the AML regulator. AUSTRAC is not a consumer-complaints body and will not help with a slow payout, but their reporting framework does catch operators who mishandle source-of-funds processes at scale. AUSTRAC’s oversight of PayID betting flows is worth understanding if you want to see where the compliance layer sits above the operator.

Finally, a practical note on weekends. The NPP rail runs 24/7, but operator review teams largely do not. A payout you request on Friday evening that hits a verification review will usually sit until Monday morning before a human looks at it. This is not a flaw in the rail or a misbehaviour by the operator. It is simply how compliance teams staff their weekends. Plan withdrawals for Monday to Thursday if you need them moving quickly, or accept the weekend pause as a known variable.