Why Your First PayID Betting Deposit Sits on a 24-Hour Hold

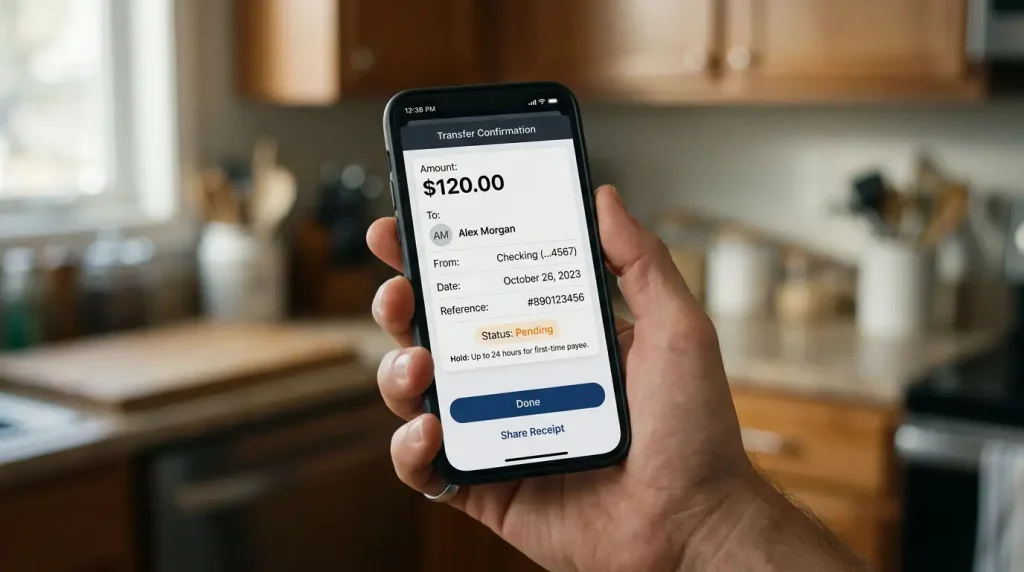

Every single week I get the same question, usually on a Saturday morning before the main racing card. “I just sent a PayID to a bookmaker. Bank says paid. Bookmaker shows nothing. What did I do wrong?” Nine times out of ten the answer is simple and annoying: nothing. The payment is sitting in a 24-hour hold that the user’s own bank silently imposes on first-time payees.

This hold catches a remarkable number of first-time PayID users off guard because nobody tells you about it up front. The cashier does not warn you. The bank app does not flag it obviously. You see “payment sent” and assume that means “funds gone”. The reality is that Australian banks sit certain outbound PayID payments behind a cooling-off window, and that window is the single most common source of “why has my deposit not landed” support tickets.

What the 24-hour hold actually is

The 24-hour new-payee hold is an anti-fraud mechanism that some Australian banks apply to outbound PayID payments when the receiving alias is brand new to your account’s payment history. The logic is straightforward. A large share of PayID-related scam losses happen when an unsuspecting user sends money to an alias they have never paid before, often under pressure from a phone call, text message, or urgent-seeming prompt. A 24-hour hold gives the sender a window to realise the mistake and cancel before the funds leave.

The hold is not a rail-level feature. The NPP itself is designed for near-instant settlement and achieves it – the rail is engineered to handle downtime of no more than around two minutes per month, so the capacity is always there. The hold is a bank-level policy that sits on top of the rail, applied at the sending bank’s discretion. Different banks apply it differently, or not at all.

Around one in four PayID users has aborted a payment mid-flow after the bank app flagged a discrepancy in the registered payee name. That statistic is the reason the hold exists. The bank’s logic is that if a quarter of users spot something wrong in the name-match step, a smaller but meaningful share of those who did not abort might realise the mistake within 24 hours. The hold is a second chance before funds move irrevocably.

The practical effect on a bookmaker deposit is the same as the cause. You send the payment, the bank shows it as sent, the bookmaker shows nothing, and the funds are quietly parked in a pending state for up to 24 hours. At the end of that window – usually earlier in practice – the bank releases the payment to the NPP rail, the bookmaker’s cashier reconciles it within seconds, and your balance updates.

Which banks apply the hold and which do not

The policy varies substantially across the market. Big-four banks tend to apply the longest default holds. Commonwealth Bank, Westpac, NAB, and ANZ all apply a hold of some duration on first payments to new PayID payees, though the exact length varies by account type, deposit amount, and the customer’s history.

In my experience the effective hold at a big-four bank for a first-time bookmaker deposit ranges from roughly one hour up to the full 24 hours. Smaller deposits – under AU$500, say – tend to clear quickly. Larger first-time deposits often sit the full window. This is a risk-scoring outcome rather than a fixed timetable.

Mid-sized mutuals and credit unions typically apply shorter holds, sometimes as little as fifteen minutes on a small first-time deposit. Neobanks sit somewhere in the middle – they process faster than the big four by default but still apply some friction on new payees. Some fintechs that participate in the NPP apply no new-payee hold at all, on the logic that the NPP’s payee-name verification is sufficient protection.

The single biggest variable, across all banks, is the context around the deposit itself. An amount that matches your usual spending pattern, sent during normal daylight hours, to an alias that cleanly resolves to a registered Australian corporate entity, will almost always clear faster than a larger, out-of-pattern transfer sent at 2am. The banks do not publish their scoring rules. They do, however, apply them consistently enough that experienced users learn the rhythm.

Scam losses from betting and sports investment frauds reached AU$2.4 million in 2025, up sharply on the prior year, with complaint volumes up close to 20%. That trend is what has kept the hold in place even as PayID adoption has scaled. Removing it would speed up legitimate deposits. It would also speed up illegitimate ones.

Legitimate ways to work around the delay

You cannot eliminate the new-payee hold as a punter, but you can shorten it significantly with some simple moves.

First, start small. Send a AU$10 or AU$20 first deposit to any new bookmaker PayID alias. Small first deposits attract less risk scoring, tend to clear faster on every bank I have tested, and establish the payee in your bank’s account history. Once the small deposit has cleared, subsequent deposits to the same alias typically land inside the usual thirty-second window because the alias is no longer new to your account.

Second, time the deposit well. A payment sent during normal business hours on a weekday will almost always clear faster than an identical payment sent late at night or on a weekend. This is partly automated risk scoring and partly the fact that human review teams are more responsive during business hours.

Third, use a bank account that matches your bookmaker KYC name exactly. If your bookmaker account is in your full legal name but the PayID alias you are sending from is registered to a business ABN or an abbreviated version of your name, the name-match check may flag the payment and extend the hold. Keep everything lined up and friction drops.

Fourth, do not try to beat the hold by sending from multiple accounts or splitting the payment. These behaviours trigger additional risk flags and can extend the hold rather than shorten it. The system is not adversarial but it does notice patterns, and spreading a deposit across five transfers looks more suspicious than sending it cleanly as one.

Fifth, pre-register the alias if your bank offers that option. Some banking apps let you save a PayID alias as a trusted payee without sending an initial payment. Where this is available, it can cut the first-time hold down materially. Check your bank’s payee management settings.

If the payment is still genuinely stuck, the escalation path is your bank first, not the bookmaker. The funds sit with your bank during the hold window, so any action to release them has to come from that side. I cover the broader diagnostic steps in more detail in the PayID deposit diagnostic checklist.

What the hold means for live betting

The hold’s most painful consequence is on live and time-sensitive markets. If you have never funded a particular bookmaker before and you decide on a Saturday afternoon to back a horse jumping in fifteen minutes, the hold can simply kill the bet.

The lesson is straightforward: do not time your first PayID deposit to a new bookmaker for a live window. Pre-fund a new account the day before, or at minimum a few hours before, you intend to use it. Once the alias is established in your bank’s history, subsequent deposits land in under a minute and you can fund with confidence right up to the jump.

For experienced punters running accounts across multiple bookmakers, the operational implication is to establish the PayID alias early at every operator you might use. A small AU$10 deposit at each new bookmaker today costs you nothing in practical terms and gives you a clean, unheld rail whenever you next want to fund that account in a hurry.

There is also a live-betting specific quirk worth knowing. Some in-play markets close very quickly – a quarter-time AFL top-up window, for instance, might be open for two minutes – and any hold at all, even a short one, means the bet does not happen. I cover in-play deposit timing on AFL and NRL live markets separately, because the rhythm is different from pre-match deposits and worth understanding on its own terms.

The single most useful habit I can recommend to any serious punter: treat the first PayID deposit to any new bookmaker as separate from the first bet. Fund. Wait. Confirm the balance. Then plan your bets. That one extra step eliminates the entire category of problem this article is about.